It only gets worse.

Through Wolf Richter to WOLF STREET.

Mortgage applications for the purchase of a home are a forward-looking indicator of where the volume of home sales will be. Sales of existing homes that closed in November have already fallen 35% year over year, 16th straight month of year-over-year declines, leading to historic plunge. And mortgage applications went in the wrong direction from there, despite falling mortgage rates.

Mortgage applications to buy a home have fallen to their lowest level since Christmas week 2014, and beyond the lows of 2014 we have to go back to 1995, according to data from the Mortgage Bankers Association today. today.

Compared to a year ago, mortgage purchase applications fell by 44%. Even during Housing Bust 1, mortgage applications didn’t drop much year over year.

This small drop in mortgage rates had no impact. This decline in mortgage applications occurred despite the decline in mortgage rates which started in mid-November from the 7.1% range and bottomed out in mid-December at 6.28. %. In the last reporting week, the average 30-year fixed rate was 6.42%, according to the Mortgage Bankers Association today.

The decline in mortgage applications indicates that it does not matter to the volume of home purchases whether the 30-year fixed rate is 6.3% or 7.1%. The difference is only cosmetic. Current house prices – although they have fallen in many markets, and fell sharply in some markets – are still simply too high.

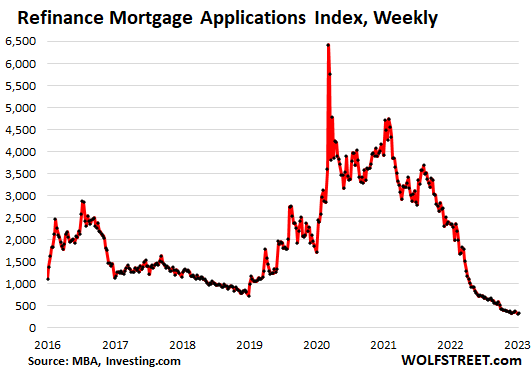

Mortgage refinance volume is dead: Mortgage refinance applications are down 86% from a year ago, despite the unseen slight rise in the past week. Since October, refinance requests have reached the lowest levels since 2000. And that makes sense, because hardly anyone would refinance a 3% or 4% mortgage with a 6% or 7% mortgage, except under duress to extract money.

The woes of mortgage lenders.

Mortgage lenders, whose revenues have collapsed as the volume of mortgage applications have collapsed, have spent the last 12 months laying off people and closing divisions. Some small operations have closed completely.

Wells Fargo, once the largest overall mortgage lender and then the largest bank mortgage lender, is the latest to make headlines with its further efforts to exit the mortgage market, on top of steps it took in 2022. .

CNBC reported yesterday that it had ‘learned’ that the bank would henceforth refocus its mortgage business solely on its existing banking and wealth management clients, and on borrowers from minority communities; that he closes his business that buys mortgages that had been issued by third-party lenders; and that it is “significantly” reducing its portfolio of mortgage services through the sale of assets. All of this will lead to another round of layoffs, in addition to layoffs in its mortgage business that began in April last year.

Wells Fargo only had about 18,000 mortgages in its retail origination pipeline in the first weeks of the fourth quarter, which was down 90% from a year earlier, according to CNBC, citing people knowing the numbers of the company.

Wells Fargo shares are down 29% from their recent high in February 2022 and 36% from their all-time high in January 2018.

The mortgage lenders that overtook Wells Fargo a few years ago weren’t banks – they were aggressive about getting mortgages in the era of easy money, then got crushed and in 2022 entered my pantheon of Imploded stocks. They all laid off large numbers of workers and some closed entire units to survive.

Their stocks have plummeted from their highs:

- Rocket Companies (owns Quicken Loans): -81%

- United Wholesale Mortgage (owns United Shore Financial): -73%

- LoanDeposit: -94%

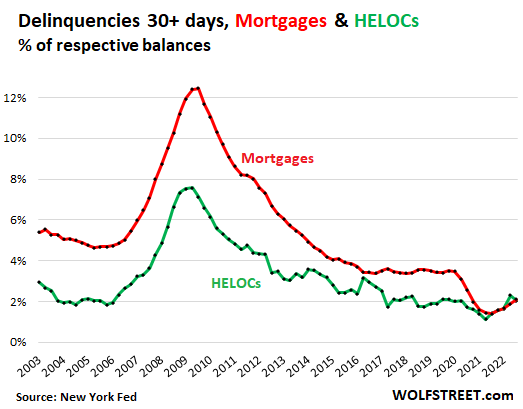

But mortgage delinquencies and foreclosures are still near their lowest levels.

What the real estate and mortgage sectors lament is the fall in the volume of home purchases and the fall in the volume of mortgage originations, which have caused their incomes to collapse.

The problem is not the credit quality of existing mortgages. At least not yet; this phase may come later if and when unemployment reaches high levels, which just isn’t happening yet despite layoffs in tech, social media and finance. Mortgage and HELOC delinquencies, although rising from record highs during the pandemic, remain very low.

The 30-plus-day HELOC delinquency rate fell to 2.0% in the third quarter of 2022, consistent with boom-period lows, according to New York Fed data (green line).

The 30+ day mortgage delinquency rate reached 2.1% (red line), still well below pre-pandemic levels.

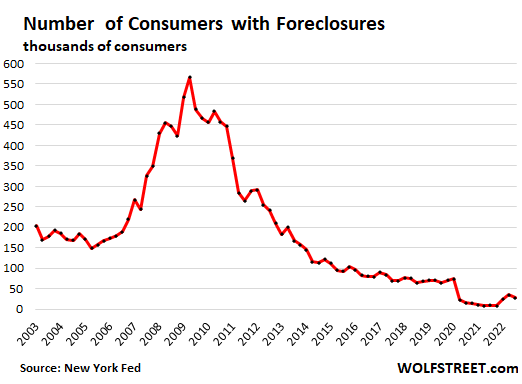

Foreclosures fell again in the third quarter to just 28,500 mortgages with foreclosures, and remain well below the number during the pre-pandemic boom, when there were around 70,000 mortgages with foreclosures:

Do you like to read WOLF STREET and want to support it? You can donate. I greatly appreciate it. Click on the mug of beer and iced tea to find out how:

Would you like to be notified by e-mail when WOLF STREET publishes a new article? Register here.

![]()

Comments are closed.